In my

introductory post on the Renewable Portfolio Standard (RPS) in NH, I

provided some basic information on RPS programs, how they work, and what renewable

energy credits (RECs) are. In this post, I take a deeper look into the buying

and selling of RECs and their pricing.

In

Part 1, I

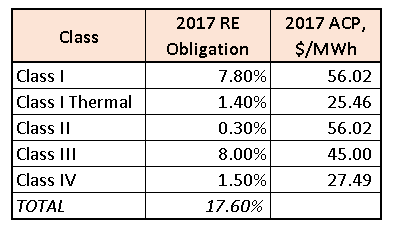

noted that there were four classes of RECs in NH (see the figure below). Classes

I and II are for the newer RE technologies and those operations that have come

on-line since 2006. Class II is dedicated to solar power alone. Classes III and

IV are for older biomass and smaller hydro operations that were established

before the end of 2005. NH is unique in that it is the first state to have

developed a sub-class and specifications for thermal RECs. These RECs are distinctive

because they don’t involve the generation of electricity, but instead involve

electricity savings via renewable energy sources such as the installation of a

solar hot water heater, geothermal system or a wood fired boiler.

Carve outs such as

those for solar and thermal are useful as they create specific requirements for

a particular type of renewable energy and prevents a flood of RECs from another

source, such as a large wind or biomass project or even out of state generation,

from driving down REC prices in these special classes

In 2017, the total NH requirement for renewable energy is 17.60%

of total electricity generation. The amount for each class, along with their

Alternative Compliance Payment (ACP), is shown in the table below. As I noted

in my

previous post, the ACP sets an upper limit – a price cap – on what the utilities are

required to pay for each REC. If prices of RECs are above the ACP, the

utilities are obligated to pay the ACP instead. When there is a shortage of REC in a specific class,

their prices quickly rise up to the ACP value set for that class; when a surplus

occurs, REC prices can drop way below the ACP.

The allocation between the different classes is

interesting. The NH program, similar to those in many other states, has a heavy

weighting to newer renewable energy generation operations in Class I, but there is also (naturally,

for a tree-covered state) a hefty weighing to Class III to support and

subsidize the pre-2016 biomass electric generators in NH. The support for solar

via Class II, is, compared to some other states, like Massachusetts, minimal.

When the RPS plan was first implemented in 2008, a steady

ramp-up in the amount of renewable energy was anticipated, from 4% in 2008 to

24.8% in 2025. Instead, there have been some important modifications to the

requirements of the various classes. From 2012 to 2016, the amount of renewable

energy from Class III was significantly curtailed to cope with the shortage of Class

III RECs. The reasoning was that a shortage of available Class III RECs would

drive the utilities to pay the ACP instead and, with the large requirement for

Class III and the high ACP payments, the costs to ratepayers would be too high.

The figure below shows how the amounts for the different

classes have changed over time. Generally, the heavy weightings of Class I and

Class III are clear and the big dip created by the reduction in the Class III

obligation from 2012 to 2016 is obvious. In 2017, the Class III requirement

zooms up from 0.5 to 8% again and the total renewable energy obligations are

back on track to meet the 2025 goal.

Different states have different RPS goals, classes, and

requirements for different types of renewable energy. For example, Maine

promotes biomass and has a high biomass requirement and Vermont includes large-scale

hydro. Each state has different ACP caps for their different classes.

Complications arise as RECs generated in one state can qualify to meet another state’s

REC requirements. Moreover, RECs qualifying in one state for a specific class

can qualify as another class in another state. This creates a New England market for RECs

but also a complicated mess due to the inconsistency in intra-state,

inter-class transactions that can occur. According

to ISO-NE the “regional REC market is not a true regional market due

to the lack of uniformity and consistent price caps”.

The result is that high ACPs, and thus high REC prices, in one state can draw in RECs from a neighboring state, thereby raising prices in the REC export state. For example, RECs from the older NH biomass operations, i.e., NH Class III, qualify as Class I in Connecticut (CT), so if REC prices in CT are high, NH Class III generators will sell their REC into the CT market instead of NH. For a number of years, CT had an enormous Class I REC requirement, which drove regional REC prices high – close to $55 (the CT ACP level). As a result, CT became a REC black hole, sucking in RECs from other New England states, including NH Class III generated RECs. This drove up regional Class I REC prices, as well as those for the NH Class III RECs. This situation created the shortage of NH Class III RECs referred to earlier and prompted the NH Public Utilities Commission to change the Class III requirements over the 2012–2016 period.

The result is that high ACPs, and thus high REC prices, in one state can draw in RECs from a neighboring state, thereby raising prices in the REC export state. For example, RECs from the older NH biomass operations, i.e., NH Class III, qualify as Class I in Connecticut (CT), so if REC prices in CT are high, NH Class III generators will sell their REC into the CT market instead of NH. For a number of years, CT had an enormous Class I REC requirement, which drove regional REC prices high – close to $55 (the CT ACP level). As a result, CT became a REC black hole, sucking in RECs from other New England states, including NH Class III generated RECs. This drove up regional Class I REC prices, as well as those for the NH Class III RECs. This situation created the shortage of NH Class III RECs referred to earlier and prompted the NH Public Utilities Commission to change the Class III requirements over the 2012–2016 period.

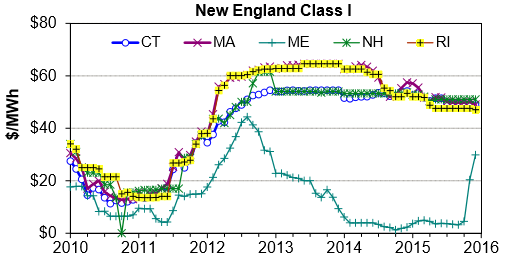

As shown in the chart below, Class I REC prices were, for a number of years, right around $55, which is the CT and NH ACP value. Massachusetts and Rhode Island prices were higher for a while, reflecting their higher ACPs. Biomass from Maine did not qualify in other states and the large volume of available biomass kept Maine Class I prices low. This chart only shows information until the end of 2015.

Source: Berkeley Lab

Source: Karbone

It should be noted that REC banking is permitted, which allows electricity suppliers to take advantage of low prices to purchase RECs for use in subsequent years. REC banking rules differ from state to state: for NH, 70% of RECs used to meet a specific RE obligation must be from current year of production, but unused RECs can be used for a further two years.

This post has provided some information about the changing REC obligations in New Hampshire especially those in Class III, and current REC pricing. This will provide a good starting point for future posts, in which I will be taking a closer look at money flows in the RPS program, as well as the implications associated with that big ramp up in Class III requirements that NH is facing in 2017.

Until my next post, do your bit to reduce our needs for electricity and RECs by remembering to turn off the lights when you leave the room.

Mike Mooiman

Franklin Pierce University

mooimanm@franklinpierce.edu

No comments:

Post a Comment

Please feel free to comment but note that I have added a verification step to avoid the large amount of spam that can make its way into the comment area. An annoying but necessary step these days.